Andrew Youderian • September 30, 2013

Andrew Youderian • September 30, 2013 The income statement seems straightforward enough: revenue at the top, expenses in the middle and profit at the bottom, right? Sadly, the good old profit-and-loss gets botched more than just about any other financial statement.

If you’re running your own business, it’s important to know what goes where. And if you’d ever like to buy or sell a store, it’s even more important to understand what goes on an income statement and how the statement should be structured so you can spot financial shenanigans and not overpay for a business.

Fortunately, there are just a few important things you need to know, all of which can be learned quickly, even if you cringe at the word “accounting.”

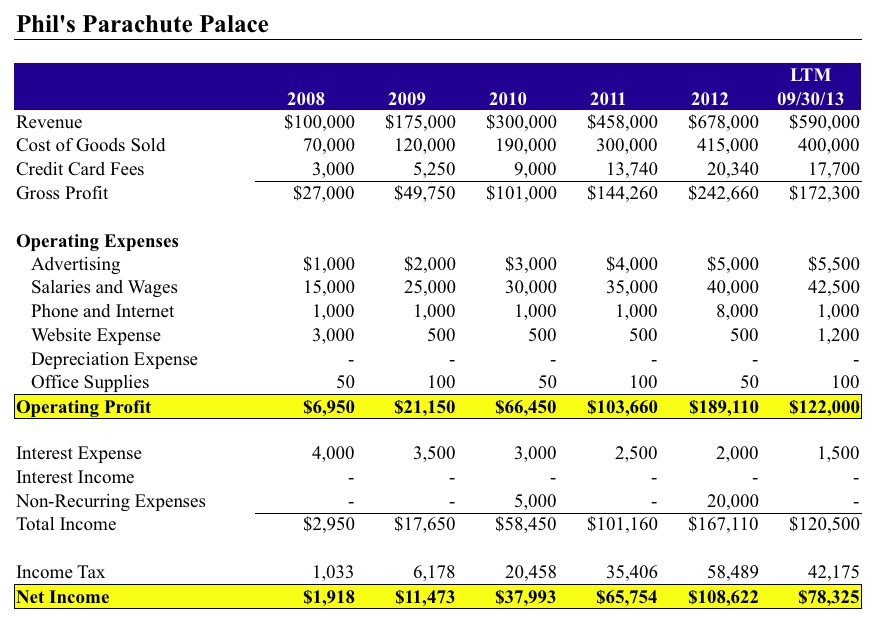

Today I’ll be walking you through the right way to format an income statement using Phil’s Parachute Palace (not real), where my friend Phil drop ships skydiving parachutes (not recommended). Let’s see how Phil’s done over the last few years:

Two Concepts to Understand

1) An income statement always represents a period of time like a month, quarter or a year. This contrasts with a balance sheet, which shows account balances for one exact date. The income statement above shows five full calendar years plus a last twelve months (LTM) period as of 9/30/13.

2) Income statements can be generated using the cash or accrual accounting method.

Cash accounting means you calculate your profits (or loss) based on when the income and expenses hit your bank accounts. Accrual accounting computes your income based on when a sale was actually made regardless of payment. So if you made a sale in January but don’t receive the funds until February, the revenue will show up in your January income statement with accrual accounting.

Accrual accounting is the most accurate, but it can be a big headache to do properly. That’s why the majority of smaller independent merchants opt for cash-based accounting.

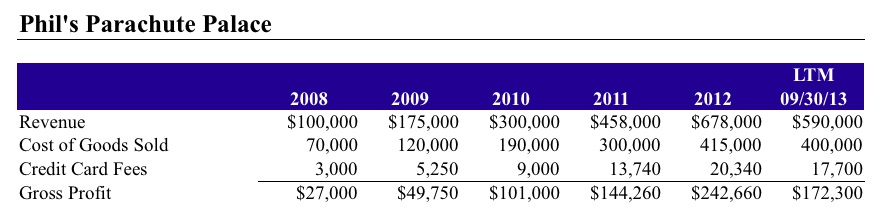

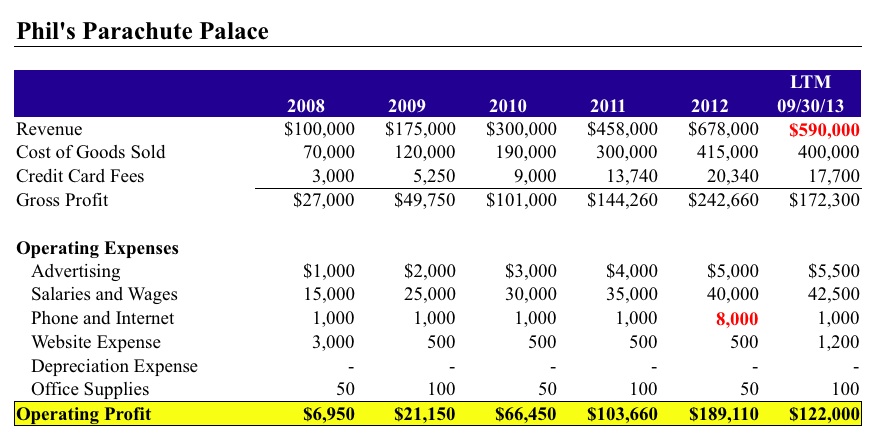

Calculating Gross Profit

The gross profit equation is:

Gross Profit = Revenue – Cost of Goods Sold – Other Direct Expenses

Gross profit is the profit remaining after paying your direct product costs but before paying for your overhead and general expenses. So for the Parachute Palace, it’s the profit Phil generated after paying for the wholesale cost of the parachute he sold.

The wholesale cost of the parachutes is referred to in accounting lingo as the Cost of Good Sold. If you want to really geek out and impress some CPAs, you can even shorten it to COGS, a term you may have seen before.

When calculating gross profit, it’s also important to consider any other expenses directly related to selling the product. For an eCommerce merchant, one obvious expense is credit card processing fees. These fees are a direct result of each sale and need to be incorporated into the gross profit.

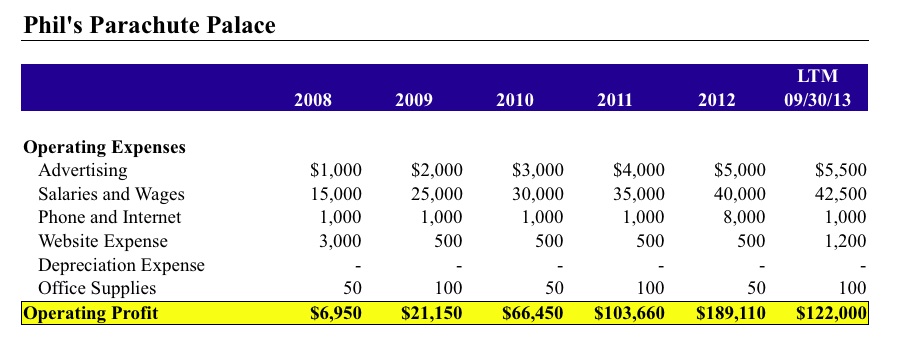

Calculating Operating Profit

Operating profit is used to determine how much money the company is bringing in from normal, ongoing operations. The operation profit formula is:

Operating Profit = Gross Profit – Overhead Expenses

Overhead includes all expenses that can’t be directly related to building/buying a product but are required to run the business: things like internet, web hosting, salaries, office suppliers and mini office basketball hoops. It all gets lumped in there.

Most of the line items are self-explanatory with the exception of depreciation. When you make a large purchase that will be used in the business over the course of many years – like a fleet of cars – you don’t claim the entire cost as an expense the first year. Instead, you write off a portion of the cost, called depreciation, each year.

Depreciation helps companies spread out the cost of large purchases over an extended time period to match the expense of the asset to its useful life. Phil drop ships all of his parachutes and doesn’t have any large purchases to depreciate, so his depreciation expenses are zero.

The reality is that most independent eCommerce merchants won’t have any depreciation expense. Even those with larger purchases they could depreciate may choose to expense them all in one year due to IRS Section 179, which allows for up to a $500,000 exception – at least in 2013. But it’s a good concept to know and understand regardless.

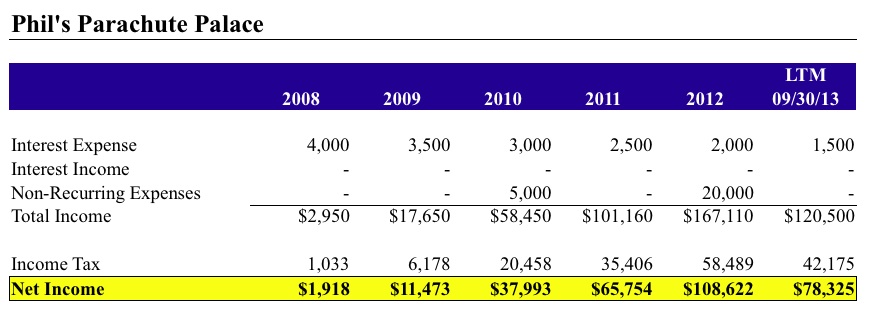

Calculating Total Income

Our last section – calculating total income – takes into account how all the non-core aspects of the business impact the bottom line.

Interest Expense – Phil took out a loan to start selling his parachutes, so he’s incurred an interest charge each year. But interest isn’t included in the operating expenses because it’s not a core expense of running the business. It’s related to how the business is financed, but doesn’t have any impact on the business’s ability to generate income.

If the business was purchased by someone else, those financing and interest expenses wouldn’t be there; they’d be different based on new financing or nonexistent if the new owner bought the business outright. So we want to isolate them, as they’re not related to the core operations.

Interest Income – For similar reasons, we want to exclude any interest income the business is generating.

Most business are purchased on a cash-free/debt-free basis, which means a a sold business won’t have excess cash or debt attached to it. An owner would pay off his loan before transferring the business and would withdraw any excess cash deposits before completing the sale.

So if a business is generating a lot of interest income from excess deposits (not likely, thanks Ben!), it doesn’t make sense to count those earnings in the operating income. A new owner wouldn’t expect to get those same interest payments as the cash hoard generating them probably wouldn’t be included in the sale.

Non-Recurring Expenses – Also along the same lines, we want to strip out any unusual profits or expenses from our operating income, which is why we include them in this section.

In 2010, Phil sadly lost $5,000 to fraud when someone claiming to be Evel Knievel purchased a bunch of parachutes with a bad check. And in 2012, Phil had to pay $20,000 to avoid a lawsuit when someone’s parachute didn’t open immediately, causing extreme terror and distress. (As I mentioned, probably not the best niche market to get into if you’re brainstorming ideas.)

Ultimately, this section isolates non-operational costs from the operational income. Because companies are valued on a multiple of their core operating earnings, getting these expenses categorized correctly can help you get a lot more for your business when selling or prevent you from overpaying when buying.

Income Tax and Net Income

The final line item before net income is income taxes. Taxes are an inevitable aspect of life and business, but you’ll almost never see them on an income statement for an independent eCommerce business.

Why? Because most independent eCommerce entrepreneurs (in the US, at least) will be set up as an LLC or an S-Corp, where business income flows through to the owner’s personal income statement to be taxed. These tax rates will vary widely from person to person, so it doesn’t make sense to include those figures along with the business financials.

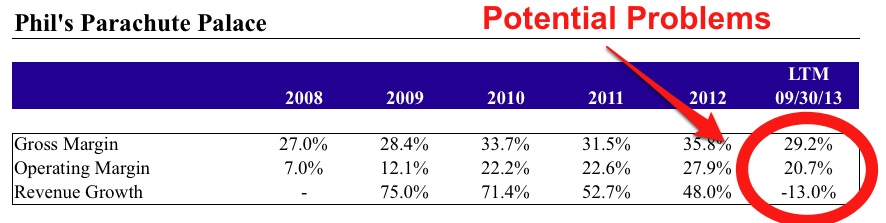

Spotting Trouble

If you’re ever considering buying a company, the due diligence process – that is, digging into the financial and bank records to make sure everything looks legitimate – is always an involved process. But there’s a lot you can learn just by quickly glancing over an income statement.

The biggest thing you want to look for is established trends that have been broken. For example, in Phil’s books below the spike in phone and internet expenses from $1,000 per year to $8,000 per year stands out like a sore thumb. Also, I’d be very curious to know why after five years of consistent growth, revenues from the last twelve months (LTM) dropped significantly.

Some items, like the dramatic increase in internet expense, are fairly easy to spot. But it can be harder to spot deeper trends from the raw numbers unless you calculate a few metrics. Two of my favorite metrics to look at are gross margin and operating margin:

Gross Margin = Gross Profit / Revenues. This metric will give you a sense of how well a company is controlling direct costs. If the number is constant or steadily increasing over time, that’s a great sign. But if it drops, make sure you understand why.

Operating Margin = Operating Profit / Revenue. Possibly the most important margin for the business, it tells how well a company is controlling all of its costs including overhead. It’s possible for a business to increase profits while its operating margin deteriorates simply by growing revenues quickly enough. Without examining the operating margin, you’d never know something was amiss.

Takeaways

So what are the most important takeaways?

Make sure variable costs are always incorporated into the gross profit. Strip out any interest or non-recurring expenses from operating income. And make sure to look for unusual trends and changes in gross and operating margin to spot red flags.

Next time I’ll be tackling an even more misunderstood financial document: the balance sheet! Until then, I’m happy to answer any questions in the comments below.

Post by Andrew Youderian